Can You Buy a House With 0 Down

Can you buy a house with no money downward?

A no–down–payment mortgage allows get-go–time home buyers and repeat habitation buyers to purchase property with no money required at closing, except standard closing costs.

Other options, including the FHA loan, the HomeReady mortgage, and the Conventional 97 loan, offer low down payment options with a little as 3% downwardly. Mortgage insurance premiums typically accompany low and no down payment mortgages, but non always.

Furthermore, mortgage rates are still low.

Rates for 30–year loans, 15–year loans, and v–year ARMs are historically inexpensive, which has lowered the monthly cost of owning a home.

Click to run across your Cipher down eligibility (Feb 17th, 2022)In this commodity (Skip to...)

- Buying with no money

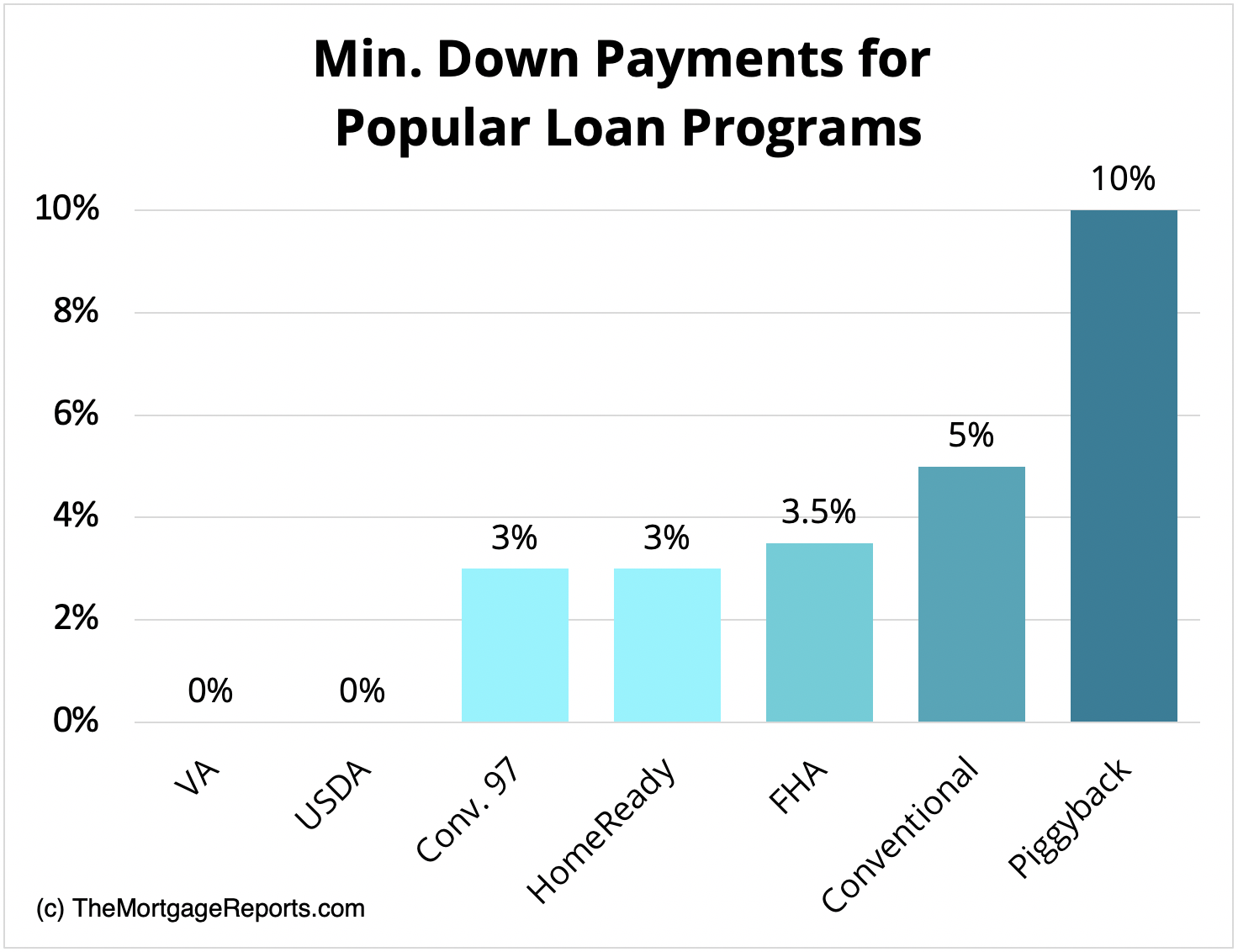

- USDA loans (0% down)

- VA loans (0% down)

- FHA loans (3.5% down)

- HomeReady loan (iii% down)

- Conventional 97 (3% down)

- Conventional (5% down)

- Piggyback Loan (x% down)

- Should yous put 20% down?

- Down payment FAQ

How to buy a firm with no money

If y'all want to purchase a firm with no money, there are ii big expenses y'all'll need covered: the down payment and endmost costs. Both can be avoided if you authorize for a null–down mortgage and/or a habitation buyer help program.

V strategies to purchase a firm with no coin include:

- Apply for a aught–down VA loan or USDA loan

- Use downwards payment assistance to comprehend the down payment

- Ask for a down payment gift from a family fellow member

- Get the lender to pay your closing costs ("lender credits")

- Get the seller to pay your endmost costs ("seller concessions")

When combined, these tactics could put yous in a new dwelling house with $0 out of pocket.

Or y'all might go your down payment covered, and then you'd but need to pay closing costs out of pocket – which could reduce your greenbacks requirement by thousands.

Verify your depression- or no-money-downwards eligibility (Feb 17th, 2022)First–time home heir-apparent loans with zero down

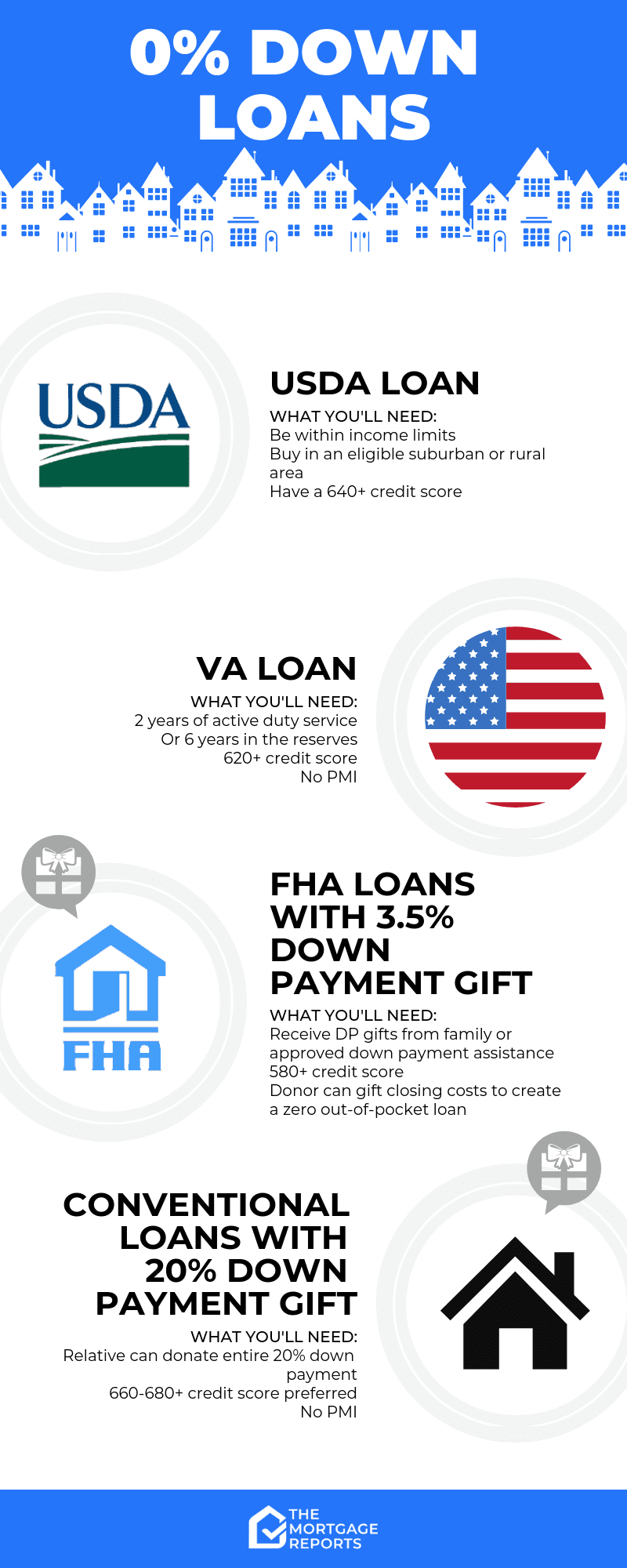

There are just 2 major loan programs with zero down: the USDA loan and the VA loan. Both are available to first–time home buyers and repeat buyers akin. But they have special eligibility requirements to qualify.

No down payment: USDA loans (100% financing)

The U.Southward. Department of Agronomics offers a 100% financing mortgage. The programme is known as the 'Rural Housing Loan' or simply 'USDA loan.'

The skilful news about the USDA Rural Housing Loan is that it'southward not but a "rural loan" – it's bachelor to buyers in suburban neighborhoods, likewise. The USDA'southward goal is to help "low–to–moderate income homebuyers," wherever they may be.

Many borrowers using the USDA loan program make a skillful living and reside in neighborhoods that don't meet the traditional definition of a 'rural area.'

Some fundamental benefits of the USDA loan are:

- No downwardly payment requirement

- No maximum habitation purchase price

- Below–market interest rates

- The upfront guarantee fee can be added to the loan residue at endmost

- Monthly mortgage insurance fees are cheaper than for FHA

Simply be aware that USDA enforces income limits; your household income must exist nigh or below the median for your surface area.

Another central benefit is that USDA mortgage rates are oftentimes lower than rates for comparable low– or no– downwardly–payment mortgages. Financing a habitation via USDA tin be the lowest–cost path to homeownership.

Check my USDA eligibility (February 17th, 2022)No downward payment: VA loans (100% financing)

The VA loan is a no–down–payment mortgage available to members of the U.South. military, veterans, and surviving spouses.

VA loans are backed by the U.South. Department of Veterans Affairs. That means they have lower rates and easier requirements for borrowers who meet VA mortgage guidelines.

VA loan qualifications are straightforward.

Most veterans, agile–duty service members, and honorably discharged service personnel are eligible for the VA program. In add-on, home buyers who accept spent at to the lowest degree vi years in the Reserves or National Guard are eligible, as are spouses of service members killed in the line of duty.

Some key benefits of the VA loan are:

- No down payment requirement

- Flexible credit score minimums

- Below–market place mortgage rates

- Defalcation and other derogatory credit information does not immediately disqualify y'all

- No mortgage insurance is required, only a one–time funding fee which can be included in the loan corporeality

In addition, VA loans have no maximum loan corporeality. It's possible to get a VA loan above current befitting loan limits, as long as y'all have strong enough credit and y'all tin afford the payments.

Check my VA loan eligibility (February 17th, 2022)Depression downwardly payment get-go–time home heir-apparent loans

Not everyone will authorize for a aught–down mortgage. Simply information technology may nevertheless exist possible to buy a house with no money down by choosing a low–down–payment mortgage and using an help plan to comprehend your upfront costs.

If you want to go this route, here are a few of the best low–money–down mortgages to consider.

Low downward payment: FHA loans (3.5% down)

The 'FHA mortgage' is a bit of a misnomer because the Federal Housing Administration (FHA) doesn't actually lend money.

Rather, the FHA sets basic lending requirements and insures these loans once they're made. The loans themselves are offered by nearly all private mortgage lenders.

FHA mortgage guidelines are famous for their liberal approach to credit scores and down payments.

The FHA volition typically insure home loans for borrowers with depression credit scores, so long as in that location's a reasonable explanation for the depression FICO.

FHA also allows a down payment of just 3.v% in all U.Southward. markets, with the exception of a few FHA approved condos.

Other benefits of an FHA loan are:

- Your down payment may come up entirely from souvenir funds or down payment assistance

- The minimum credit score is 500 with a 10% down payment, or 580 with a 3.5% down payment

- Upfront mortgage insurance premiums tin exist included in the loan amount

Furthermore, the FHA can sometimes help homeowners who take experienced recent short sales, foreclosures, or bankruptcies.

The FHA insures loan sizes upwardly to $ in designated "loftier–cost" areas nationwide. High–price areas include places similar Orange County, California; the Washington D.C. metro area; and, New York Metropolis's 5 boroughs.

Notation that if you lot want to use an FHA loan, the home being purchased must be your chief residence. This program isn't intended for holiday homes or investment properties.

Click to run across your 3.5% down FHA eligibility (Feb 17th, 2022)Depression downwards payment: The HomeReady Mortgage (3% down)

The HomeReady mortgage is special among today'due south depression– and no–down–payment mortgages.

Backed by Fannie Mae and available from nearly every U.S. lender, the HomeReady mortgage offers beneath–marketplace mortgage rates, reduced private mortgage insurance (PMI) costs, and innovative underwriting for lower–income home buyers.

Via HomeReady, the income of everybody living in the home can be used to get mortgage–qualified and approved.

For example, if you are a homeowner living with your parents, and your parents earn an income, y'all can utilise their income to help you qualify.

The HomeReady plan also lets yous utilize boarder income to help authorize, and you can use income from a not–zoned rental unit of measurement, too – even if you lot're paid in greenbacks.

HomeReady abode loans were designed to help multi–generational households go approved for mortgage financing. Even so, the programme can be used by anyone in a qualifying area, or who meets household income requirements.

Freddie Mac offers a like program, called Dwelling Possible, which is also worth a look.

Home Possible is a little less flexible nearly income qualification than HomeReady. But it offers many like benefits, including a minimum three% downwardly payment.

Click to meet your 3% downward eligibility (Feb 17th, 2022)Low down payment: Conventional loan 97 (3% down)

The Conventional 97 programme is available from Fannie Mae and Freddie Mac. Information technology'south a 3% downwards payment programme and, for many home buyers, it'south a less expensive loan selection than an FHA mortgage.

Bones qualification requirements for a Conventional 97 loan include:

- Loan size may non exceed $, even if the dwelling is in a high–cost market

- The belongings must be a single–unit of measurement dwelling. No multi–unit of measurement homes are allowed

- The mortgage must be a fixed–rate mortgage. No adaptable–rate mortgages are allowed via the Conventional 97

The Conventional 97 program does not enforce a specific minimum credit score across those for a typical conventional home loan. The program can be used to refinance a domicile loan, likewise.

In addition, the Conventional 97 mortgage allows for the entire 3% down payment to come from gifted funds, and so long as the gifter is related by blood or marriage, legal guardianship, domestic partnership, or is a fiance/fiancee.

Low down payment: Conventional mortgage (5% down)

Conventional 97 loans are a little more restrictive than 'standard' conventional loans, considering they're intended for first–fourth dimension home buyers who need extra help qualifying.

If you don't meet the guidelines for a Conventional 97 loan, you lot tin salvage up a trivial more and try for a standard conventional mortgage.

Conventional mortgages are the most popular loan type in the marketplace because they're incredibly flexible. Yous can make a downward payment as low as 5% or as big as 20%. And you only need a 620 credit score to authorize in many cases.

Plus, conventional loan limits are higher than FHA loan limits. And so if your purchase price exceeds FHA'southward limit, yous might want to save upwards 5% and endeavour for a conventional loan instead.

Conventional mortgages with less than twenty% down require private mortgage insurance (PMI). But this can be canceled once you have xx pct equity in the habitation. So you're not stuck with the additional fee forever.

Verify your conventional loan eligibility (February 17th, 2022)Depression downwards payment: The "Piggyback Loan" (10% down)

One terminal option if you want to put less than 20% down on a house – only don't want to pay mortgage insurance – is a piggyback loan.

The "piggyback loan" or "80/10/x" program is typically reserved for buyers with above–boilerplate credit scores. It'south really iiloans, meant to give home buyers added flexibility and lower overall payments.

The beauty of the 80/10/x is its structure.

- With an 80/10/10 loan, buyers bring a 10% down payment to closing

- They also get a 10% 2d mortgage (HEL or HELOC)

- This leaves an 80% mortgage loan

- Since y'all're finer putting 20% down, there is no PMI

The first mortgage is typically a conventional loan via Fannie Mae or Freddie Mac, and it'southward offered at current market mortgage rates.

The second mortgage is a loan for x% of the home's purchase price. This loan is typically a abode equity loan (HEL) or dwelling equity line of credit (HELOC).

And that leaves the last "10," which represents the buyer's down payment amount – x% of the purchase price. This amount is paid equally cash at closing.

This type of loan structure can assist you lot avoid private mortgage insurance, lower your monthly mortgage payments, or avoid a colossal loan if you're correct on the cusp of conforming loan limits.

Even so, you'll typically need a credit score of 680–700 or higher to qualify for the 2nd mortgage. And you lot'll have two monthly payments instead of one.

If you're interested in a piggyback mortgage, discuss pricing and eligibility with a lender. Make sure you're getting the virtually affordable home loan overall – month–to–month and in the long term.

Click to see your depression-downpayment loan eligibility (February 17th, 2022)Home buyers don't need to put xx% down

It's a common misconception that "20 percent down" is required to buy a home. And, while that may accept truthful at some point in history, it hasn't been so since the appearance of the FHA loan in 1934.

In today's real estate market place, home buyers don't need to make a 20% downwardly payment. Many believe that they practice, all the same – despite the obvious risks.

The likely reason buyers believe twenty% down is required is because, without 20 percent, you'll have to pay for mortgage insurance. Merely that'due south not necessarily a bad thing.

PMI is not evil

Private mortgage insurance (PMI) is neither skillful nor bad, just many dwelling house buyers still try to avoid information technology at all costs.

The purpose of individual mortgage insurance is to protect the lender in the event of foreclosure – that's all it's for. However, because information technology costs homeowners money, PMI gets a bad rap.

It shouldn't.

Because of private mortgage insurance, home buyers can become mortgage–canonical with less than 20% down. And, eventually, private mortgage insurance can be removed.

At the rate today'due south dwelling house values are increasing, a heir-apparent putting 3% down might pay PMI for fewer than 4 years.

That's not long at all. Nonetheless many buyers – especially kickoff–timers – will put off a purchase because they desire to save up twenty percent.

Meanwhile, home values are climbing.

For today's dwelling house buyers, the size of the down payment shouldn't be the just consideration.

This is because home affordability is not about the size of your down payment – it's about whether you can manage the monthly payments and still accept cash left over for "life."

A big downwardly payment will lower your loan corporeality, and therefore will requite you lot a smaller monthly mortgage payment. Yet, if you lot've depleted your life savings in order to make that large downward payment, you lot've put yourself at risk.

Don't deplete your entire savings

When the majority of your money is tied up in a habitation, financial experts refer to it as existence "firm–poor."

When yous're house–poor, y'all accept plenty of money on paper merely little cash available for everyday living expenses and emergencies.

And, as every homeowner will tell you, emergencies happen.

Roofs plummet, h2o heaters break, you become ill and cannot piece of work. Insurance tin help y'all with these issues sometimes, but not ever.

That'due south why beingness house–poor is so dangerous.

Many people believe it'south financially conservative to put 20% down on a home. If 20% is all the savings you have, though, using the total amount for a down payment is the reverse of being financially conservative.

The true financially conservative option is to make a pocket-size down payment and get out yourself with some money in the banking company. Existence house–poor is no way to alive.

Click to see your ZERO down eligibility (Feb 17th, 2022)Mortgage downwardly payment FAQ

Hither are answers to some of the near frequently asked questions about mortgage downwardly payments.

What is the minimum down payment for a mortgage?

The minimum down payment varies by mortgage program. VA and USDA loans allow cypher downward payment. Conventional loans offset at iii percent down. And FHA loans require at least iii.5 percent down. You lot are free to contribute more than the minimum down payment corporeality if you want.

Are there zero-downwardly mortgage loans?

There are just ii first–fourth dimension home buyer loans with zero downwards. These are the VA loan (backed by the U.S. Department of Veterans Affairs) and the USDA loan (backed by the U.S. Department of Agriculture). Eligible borrowers can buy a house with no money down simply volition still have to pay for closing costs.

How can I buy a house with no coin down?

In that location are two ways to buy a house with no money down. One is to get a zero–downwardly USDA or VA mortgage if yous qualify. The other is to get a depression–down–payment mortgage and comprehend your upfront cost using a downwards payment assistance programme. FHA and conventional loans are available with just iii or 3.5 percent downwards, and that entire amount could come up from down payment help or a greenbacks gift.

What credit score practise I demand to purchase a house with no money down?

The no–money–downwards USDA loan plan typically requires a credit score of at least 640. Another no–money–down mortgage, the VA loan, allows credit scores every bit low every bit 580–620. Just you lot must exist a veteran or service member to qualify.

What are down payment assistance programs?

Down payment assistance programs are bachelor to home buyers nationwide, and many first–time home buyers are eligible. DPA can come in the class of a dwelling heir-apparent grant or a loan that covers your down payment and/or endmost costs. Programs vary past state, and so be sure to ask your mortgage lender which programs you may be eligible for.

Are there any dwelling buyer grants?

Home buyer grants are offered in every state, and all U.Southward. home buyers tin apply. These are besides known every bit down payment assistance (DPA) programs. DPA programs are widely available but seldom used – many habitation buyers don't know they exist. Eligibility requirements typically include having low income and a decent credit score. But guidelines vary a lot by program.

Tin cash gifts exist used as a down payment?

Yes, greenbacks gifts can exist used for a downwardly payment on a dwelling. But you must follow your lender's procedures when receiving a greenbacks gift. Outset, make certain the gift is made using a personal check, a cashier's cheque, or a wire. Second, go along paper records of the gift, including photocopies of the checks and of your deposit to the bank. And make sure your deposit matches the amount of the gift exactly. Your lender will also want to verify that the gift is actually a souvenir and not a loan in disguise. Cash gifts must not require repayment.

What are FHA loan requirements?

FHA loans typically require a credit score of 580 or higher and a three.5 pct minimum downward payment. Y'all will also need a stable income and ii–year employment history verified past Westward–two statements and paystubs, or by federal tax returns if self–employed. The dwelling house you're purchasing must exist a master residence with 1–4 units that passes an FHA domicile appraisal. And your loan amount cannot exceed local FHA loan limits. Finally, you cannot have a recent bankruptcy, foreclosure, or brusk auction.

What are the benefits of putting more money down?

Just as there are benefits to low– and no–money–down mortgages, there are benefits to putting more than money down on a home buy. For example, more money down means a smaller loan amount – which reduces your monthly mortgage payment. Additionally, if your loan requires mortgage insurance, with more than money downward, your mortgage insurance volition be removed in fewer years.

If I make a low down payment, practice I pay mortgage insurance?

Mortgage insurance is typically required with less than xx percent down, but not always. For example, the VA Home Loan Guaranty program doesn't crave mortgage insurance, so making a low down payment won't matter. Conversely, FHA and USDA loans alwaysrequire mortgage insurance. So even with large down payments, you'll have a monthly MI charge. The only loan for which your downward payment amount affects your mortgage insurance is the conventional mortgage. The smaller your down payment, the higher your monthly PMI. However, one time your home has 20 per centum equity, you'll be eligible to have your PMI removed.

If I brand a depression down payment, what are my lender fees?

Lender fees are typically adamant as a percentage of your loan corporeality. For instance, the loan origination fee might be i percent of your mortgage balance. The bigger your downwards payment, the lower your loan amount will exist. And so putting more than money downwardly can help lower your lender fees. But you'll still have to bring more cash to the closing table in the form of a down payment.

How can I fund a downward payment?

A down payment tin be funded in multiple means, and lenders are ofttimes flexible. Some of the more mutual ways to fund a down payment are to use your savings or checking business relationship, or, for echo buyers, the gain from the auction of your existing dwelling house.

However, there are other ways to fund a downwardly payment, too.

For example, habitation buyers can receive a greenbacks gift for their downward payment or borrow from their 401k or IRA (although that's not e'er wise).

Downwards payment assistance programs tin can fund a down payment, too. Typically, downward payment assistance programs loan or grant coin to home buyers with the stipulation that they alive in the home for a certain number of years – often v years or longer.

Regardless of how you fund your down payment, make sure to go along a paper trail. Without a clear account of the source of your down payment, a mortgage lender may non allow its apply.

How much home can I afford?

The answer to the question "How much abode can I afford?" is a personal one and should not be left solely to your mortgage lender.

The best style to decide how much house yous can afford is to commencement with your monthly budget and decide what y'all can comfortably pay for a home each month.

Then, using your desired payment equally the starting bespeak, use a mortgage calculator and work backward to detect your maximum home buy price.

Note that today's mortgage rates will affect your mortgage calculations, then be sure to use current mortgage rates in your estimate. When mortgage rates alter, and then does home affordability.

What are today's low–downward–payment mortgage rates?

Today's mortgage rates are low beyond the board. And many low–down–payment mortgages have below–market rates thanks to their government backing; these include FHA loans (3.5% downwards) and VA and USDA loans (0% downwards).

Different lenders offer different rates, and then yous'll want to compare a few mortgage offers to detect the best deal on your low– or no–downward–payment mortgage. You tin get started right here.

Bear witness me today'south rates (Feb 17th, 2022)

The information contained on The Mortgage Reports website is for informational purposes merely and is not an advert for products offered past Full Chalice. The views and opinions expressed herein are those of the author and do not reflect the policy or position of Full Chalice, its officers, parent, or affiliates.

Source: https://themortgagereports.com/11306/buy-a-home-with-a-low-downpayment-or-no-downpayment-at-all

0 Response to "Can You Buy a House With 0 Down"

Post a Comment